Alberta, the province that has become the epicenter of Canada’s oil bust, does not yet have a budget for fiscal 2015-16. Premier Rachel Notley promised delivery by October. But it won’t be easy. Ideas are already floating around and are getting shot down. The problem: a budget crisis has set in after a sudden shortfall of C$7 billion in oil revenue.

There have been layoffs in the oil patch. Companies are retrenching. Home prices are tumbling in Calgary, the oil capital of Canada. In May, they plunged a record 3.3% and are now down 7% from their peak seven months ago.

In commercial real estate, it’s getting ugly. The number of transactions of C$1 million or more in the first quarter plummeted by 21%, and the dollar value of transactions dropped 11%, according to RealNet Canada, cited by the Calgary Herald.

Cushman & Wakefield reported that the premium office market in Calgary is “reeling from the sudden impact of downsizing companies.” Unless a miracle happens in the oil markets that sends prices back into the stratosphere, the premium office market will see vacancy rates climb to 12.4% by the end of this year, and to 15.4% by the end of 2016, the worst since the early 1990s. In the first quarter alone, a record 1.23 million square feet of office space were put back on the market as companies, mauled by the oil-price plunge and trying to stay alive, are slashing operating expenses where they can.

With impeccable timing, a flood of new space is being built and will soon come on the market. Bob McDougall, senior managing director of brokerage for Cushman & Wakefield in Calgary, explained:

“On top of low office demand and companies subletting record amounts of space, we’re in the midst of a major development cycle with about three million square feet under construction downtown. Right now, it’s a perfect storm.”

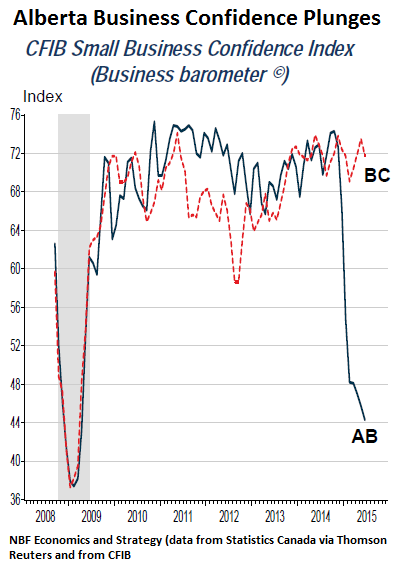

And this “perfect storm” has slammed into business confidence in Alberta, with a totally breathtaking force, as the Economics and Strategy group of National Bank Financial reported. Its chart of the CFIB small-business confidence index for Alberta (black line) and neighboring British Columbia (red line) shows “a record gap between the two provinces in June.”

And what a cliff dive small-business confidence has taken in Alberta over the past few months. In June, it hit the lowest level since the Financial Crisis in 2009:

That kind of plunge in confidence is rare. The Financial Crisis was a terrifying event for businesses. And the oil bust is having a similar effect in Alberta. It speaks of the deep turmoil and anxieties in the business community that is trying to survive somehow even while the oil bust batters their business models, revenues, profits, and balance sheets. And it speaks of the myriad side effects it has on the rest of the business community, the broader economy, and government.

So in Alberta, the “difficult conditions seem set to endure for a while longer,” wrote NBF Senior Economist Marc Pinsonneault.

But the rest of Canada seems to be fine, still: “Things are actually looking up for most of the larger provinces with Ontario, Quebec, and British Columbia carrying a good amount of momentum going into H2 2015.”

And he concludes:

All and all, the data remain consistent with our view that Alberta’s woes are not translating into a full-fledged contagion to the rest of the country. As such, we remain comfortable with our view that after a difficult start to 2015, firmer growth in Canada’s three most populous provinces is poised to offset still-mounting weakness in previously high-flying resource-levered jurisdictions.

And hopefully – the operative word – that will be the case. Because some terrific bubbles in housing and commercial real estate have bloomed into majestic maturity, particularly in Toronto and Vancouver. Household indebtedness has soared. The banks are exposed, And it wouldn’t take much of a trigger to send treacherous vibrations through the whole precarious, debt-funded construct.

“All of that negative news has kind of put a downer on consumer sentiment,” is how Jharonne Martis, director of consumer research at Thomson Reuters, explained the crummy consumer confidence reading. Read… It Gets Messy in Canada

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

The winter solstice marks the onset of winter – but the deepest cold occurs a month or two later. Too early to be declaring no contagion.

This is not a new phenomenon. I remember years ago a joke about Calgary. The only thing supposedly selling was concrete building blocks. Oil execs were using them to break their office windows so they could jump out easier.

About 6 months before the downturn my son switched from industrial electrician in the oil patch to construction ….mostly 4 story multi-family dwellings. He can’t get a day off. People need places to live and these are affordable.

There is nothing wrong with development of mega-plants/projects in the Oil Sands slowing down. There has been a shortage of workers with a corresponding influx of foreign workers to fill gaps. There has been a lack of sober evaluation of environmental concerns. There has been terrible waste and totally unrealistic expectations for wages and profits. (I know absolute idiots making $150,000/year). I know company insiders leasing trucks and equipment to the developers for huge daily rates to simply sit.

No, let it slow down and proceed slowly. If it takes a gold-rush surge to develop this industry take a drive up to Dawson or Ross River Yukon and check out depleted resource towns. Then, come home and evaluate/plan for reasonable growth and expectations.

If it booms, it always always always goes bust.

regards

Canadian real estate long passed the possibility of Soft Landing. At current level if prices, with average 600K RE transactions a year, in 5 years we will have well over 30% of the entire population living in mind-blowing debt.

Every passing year digs this pit ever deeper.

From another hand, our magnificent housing bubble is steadily killing real economy, and especially manufacturing.

No manufacturing activity may thrive in environment where industrial workers live in $500K-plus townhouses. We just cannot stay competitive! And all these suggestions that Canada should stop competing for low paying jobs with Michigan, and start competing with Massachusetts…, well, America is not even allowing Alberts to compete with Dakota, Oklahoma and Texas, so who says they gonna allow us to compete with Massachusetts? They may allow us to compete with Mexico…, if our workers agree to match Mexican wages…. (again, $750K semies come to mind…)

How does this turn out? Like it always does; decline in ‘asset’ prices => deleveraging => bank insolvency => derivative meltdown.

How do you bail out the broken banks when interest rates are zero and the ongoing bubble is fueled with bailout money?

I guess everyone is going to find out. Oil price crash that started last year is like the collapse of the Bear Stearns High-Grade Structured Credit Fund and the B-S High-Grade Structured Credit Enhanced Leveraged Fund in 2007.

There’s a double whammy in Alberta, and that’s the fact that the NDP, a socialist party has been recently elected. Coupled with the downturn in oil prices this spells big trouble; as an example, when the NDP were elected in Ontario the downslide began (and has been continued under the ‘Liberal’ Party). From being the wealthiest province in Canada Ontario now receives transfer payments from the Feds, and their debt position (as much as 300 billion dollars for 12 million people) is worse than California, the poster child for irresponsible government. In Alberta, the NDP’s environmentalist/New Age philosophy is duty-bound to attack business, and especially the oil sands business (which is operating precariously close to the breakeven or even loss-price of oil). Capital spending has declined dramatically in the oil sands, and without higher oil prices, the effect may well be catastrophic. Subsidized oil production? Anything’s possible in Canada, the dreamland. The last major government attack on the oil business was under Trudeau’s Federal Liberals’ National Energy Plan in the 1970s, with the result that gasoline prices at the government’s Petro-Canada (the slogan was something like ‘it’s the people’s oil company’) stations were always the highest and Petro-Canada managed to lose money while building itself towers in the sky filled with bureaucrats, until the whole rotten mess threatened to collapse and was finally privatized.

The last good government in Alberta was the Conservatives led by Ralph Klein (premier 1992-2006) who was ridiculed because of his homespun manner and finally thrown out of the leadership by his own party, Thatcher-style – a typical fate for successful leaders that don’t follow the entitled-victim philosophy of government; any Conservative government after him has pandered for diminishing votes by adopting opposition policies alien to the spirit of Alberta, which was a toned-down wild west sort of environment. Klein reduced government debt to zero by tough spending cuts, and actually sent residents rebate checks (the ‘Prosperity Dividend’).

Alberta is the last province of Canada to not have a provincial sales tax; will the NDP fix that? Alberta also has a Heritage Fund, created by the Conservatives in the late ’70s, funded by oil royalties. It grew to over 15 billion dollars, but has flat-lined for some years now due to excessive spending by the government, which is now well back into debt and which runs deficits rather than the surpluses of the Klein years. Look for the new government to blame everyone else rather than cut spending to suit the current circumstances. Rather than run the debt down to zero a more likely bet may be that the Heritage Fund will be run down to zero.